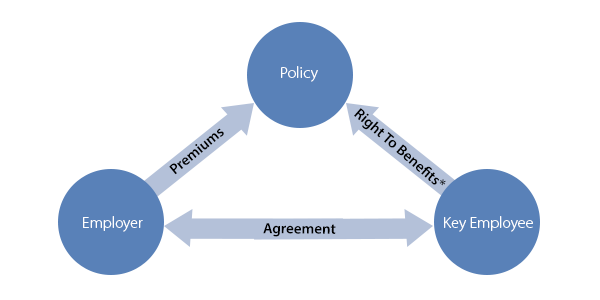

A Controlled Executive Bonus Plan, also known as a Restrictive Executive Bonus, or Section 162 plan, is an agreement between an employer and its key employee(s) to provide a death benefit, supplemental income, and now includes long-term care benefits.

The employee applies for and owns the life insurance policy, with the right to designate the beneficiary(ies) of the policy. The company then pays the “bonus” premium directly to the insurance company. The employee’s right to receive the cash value of the policy through loans, withdrawals or surrender is restricted during a time period based on age, years of service or other conditions agreed upon by the company and the employee.

If the employee terminates employment during this restricted period, the company must agree for the employee to have access to policy cash values. The employer, at that time, may require repayment of some or all of its “bonus” premiums from the policy’s cash value in exchange for its agreement.

*Subject to agreement

*Subject to agreement

A Controlled Executive Bonus Plan has two advantages to the employer:

- Pay key employee(s) a bonus in the form of a life insurance premium.

- Can take a current deduction for the bonus.

Benefits of a Controlled Executive Bonus Plan

For the employer:

- Can select which key employees can participate

- No mandatory eligibility and participation rules

- No IRS restrictions or approval

- No government forms or reports, minimal administration

- “Bonus” premiums are tax-deductible

- Recruit, reward and retain key employees using “golden handcuffs”

For the employees:

- Income-tax free benefits paid to surviving family at death

- Permanent life insurance protection

- Long-term care benefits available

- Tax-deferred growth of policy cash values

- Income-tax free death benefits

- Although the employee must report the life insurance premiums paid each year as taxable compensation, impact of this can be minimized by the employer providing a cash bonus to the employee sufficient enough to cover both the premiums and income taxes due

- Unrestricted ownership of policy and its values after the restricted period ends

The endorsement is executed by the employer and employee and filed with the insurance company. For a specified period of time agreed to by the employer and the employee, the endorsement restricts some of the employee’s ownership rights in the policy. During the restricted period, the endorsement restricts the right of the employee to surrender the policy, assign the policy as collateral, change ownership or make a policy loan, unless the employer also agrees. The restrictive endorsement is typically designed to expire at a defined point, usually between 5-15 years.

For more information about the long term care benefits included in a controlled executive bonus plan, please contact us today.